State of CVC 2025: Maturity, Mandate Shifts and the New Operating Reality

Corporate venture capital (CVC) has entered a more self-aware and structurally complex phase. As artificial intelligence reshapes corporate strategy and venture theses, CVC units are no longer experimental appendages of large enterprises—they are increasingly mature investment platforms grappling with the same pressures facing traditional venture funds: speed, talent, liquidity, and returns. The State of CVC 2025 highlights an ecosystem that is scaling in sophistication, while simultaneously confronting internal friction.

A Market Dominated by Mature Players

Nearly half (49%) of CVC funds globally are now classified as “mature,” with established investment processes and a demonstrable track record of successful startup investments. Another 43% fall into a middle stage—active for several years and increasingly confident in their mandate. Only 8% of funds are new entrants.

This maturity reflects a broader normalization of CVC as a long-term corporate capability rather than a cyclical innovation experiment. As Bloomberg has noted in recent coverage, many global corporates now view venture investing as a strategic radar for disruption, particularly in AI, climate tech, and enterprise software, rather than a purely financial exercise.

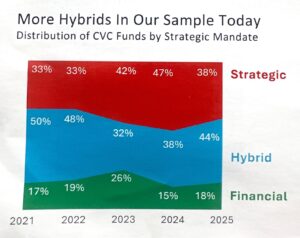

The Rise of the Hybrid Mandate

Strategic intent remains central to CVC, but the lines between strategic and financial investing are blurring. From 2021 to 2025, hybrid CVC models—funds balancing strategic alignment with financial discipline—have consistently represented the largest share of the market. In 2025, 44% of CVCs identify as hybrid, compared to 38% purely strategic and 18% primarily financial.

This shift mirrors observations by Fast Company, which has highlighted how corporates increasingly demand measurable financial performance from innovation teams. Hybrid structures allow CVCs to justify their existence internally while retaining flexibility to invest opportunistically, particularly in fast-moving AI markets where commercial applications may emerge faster than corporate integration pathways.

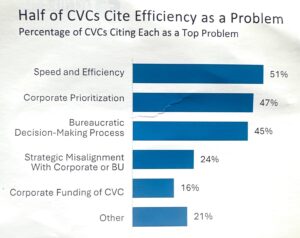

Efficiency Is the Defining Constraint

Despite increased maturity, operational friction remains the most cited challenge. In 2025, 51% of CVCs identify speed and efficiency as their top problem, followed closely by corporate prioritization (47%) and bureaucratic decision-making (45%). These constraints limit CVCs’ ability to compete for high-quality deals, especially at early stages where founders expect rapid conviction and clear governance.

This tension—between venture-speed decision-making and corporate oversight—has been widely documented. Bloomberg recently described CVCs as “structurally advantaged but operationally constrained,” noting that the very governance designed to protect corporate interests often undermines competitive execution.

Structural Separation Gains Momentum

As a result, more CVCs are questioning their operating model. One in four CVCs considered moving off the corporate balance sheet in the past year, citing compensation flexibility, investment independence, and talent retention as key drivers. However, execution remains difficult: only 11% have successfully completed such transitions to date.

Notably, financial CVCs are significantly more likely to operate off balance sheet, reinforcing the link between structural independence and investment agility. This trend reflects a broader rethinking of how corporates attract venture talent in an increasingly competitive market.

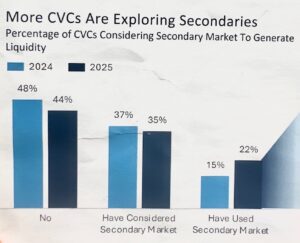

Liquidity and the Secondary Market

Liquidity is no longer a taboo topic. In 2025, 57% of CVCs report either using or actively considering the secondary market, up from the previous year. While 44% still report not engaging in secondaries, the share of funds that have actually used them rose sharply—from 15% in 2024 to 22% in 2025.

Financial CVCs lead adoption, with 41% having used secondaries, but interest is growing across strategic and hybrid funds. This reflects longer exit timelines, fewer IPOs, and corporate pressure to demonstrate realized value—trends widely echoed in Fast Company’s analysis of post-ZIRP venture markets.

Early-Stage Appetite and the AI Effect

Finally, CVCs are leaning earlier. Seed and early-stage investments now account for over 67% of CVC deal activity, up from 55% a decade ago. AI dominates this shift: 28% of all CVC deals in 2025 involve AI companies, compared to just 9% in 2015.

This underscores a defining paradox of modern CVC: while funds struggle with internal speed and structure, they are simultaneously more willing than ever to back nascent, high-risk technologies. The result is an ecosystem that is strategically ambitious—but operationally under pressure.

Looking ahead, the state of CVC in 2025 is not one of retreat, but recalibration. The next phase will be defined not by capital availability, but by governance innovation—how corporates redesign venture units to move faster, think longer-term, and compete on equal footing with traditional VCs.

Subscribe to our Newsletter

Join our mailing list for exclusive updates and promotions!